Ten macroeconomic points to keep in mind this week

1 – The IMF has revised on the downside its forecast. In 2015 the world GDP will grow by 3.1% after 3.4% in 2014. Expectations for 2016 are marginally higher at 3.6%.

The main reason is in emerging countries which suffer with low commodity prices and the persistent weaker dynamics seen in China. The other point of concern is associated with higher Fed’s rates in the US. We feel a worried environment at this meeting

2 – The signature of the Trans-Pacific Partnership (or TPP) between the USA and 11 Asian partners (without China) is important. It is supposed to boost trade between all these members but we don’t know exactly what will happen in the balance of strength in this new framework. The arbitrage in case of conflict will be done by the World Trade Organization but we know that the role of states and companies will be different. This could be directly seen on the labor market conditions. As negotiations have been secret we need more details to clearly see the global picture and we will see with the experience how this TPP will work.

The agreement was a target for the current US administration and for Asian countries it’s a way to improve their relationship with the US in a period during which Chinese momentum is weaker. All these countries that became dependent on the Chinese dynamics can expect an improvement of their trade.

3 – From central banks’ minutes we perceived that the global situation is not strong yet. The postponement of the convergence of inflation to their target of 2% and the limited growth momentum they perceive are a source of concern. They prefer waiting instead of acting in a too early manner.

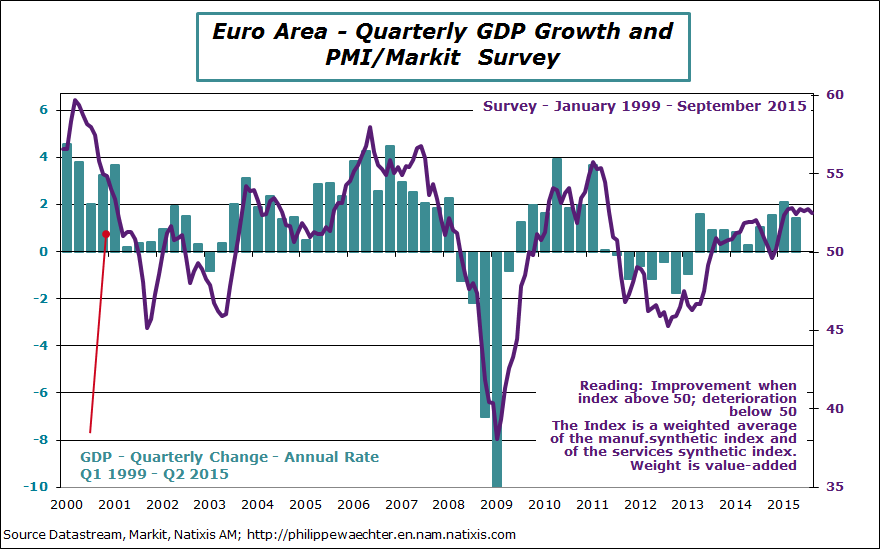

4 – The Markit synthetic index for the Euro Area has been revised on the downside but its level is still in the corridor seen since last February. Growth will be positive in 2015, there is no ambiguity, but it doesn’t accelerate. Countries’ business cycles are still too heterogeneous.

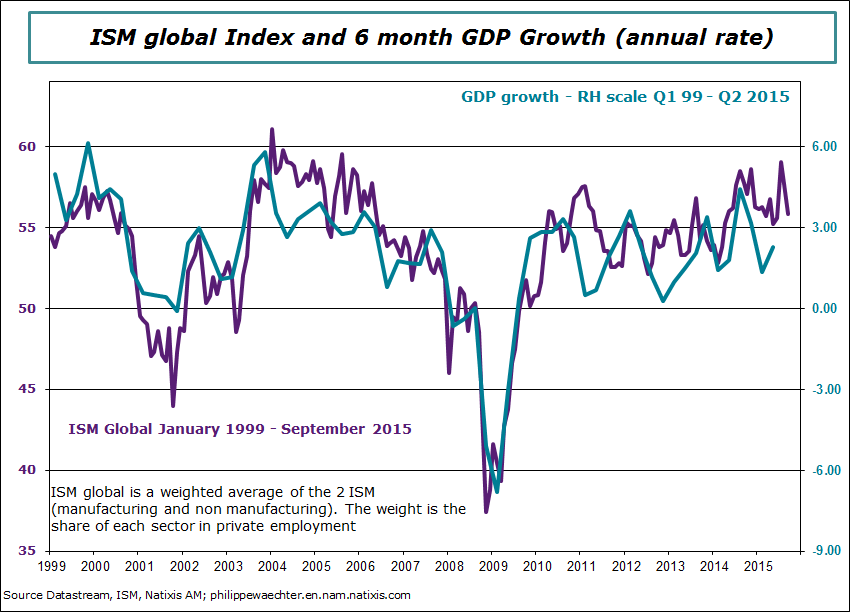

5 – The ISM global index, which is a weighted average of the two ISM index (manufacturing and non-manufacturing), has a lower momentum in September. The manufacturing index was low at 50.2 and the non-manufacturing index dropped compared to the recent peak of July. On the graph, the trend is flat but consistent with a positive growth. The Fed was right in doing nothing in September.

5 – The ISM global index, which is a weighted average of the two ISM index (manufacturing and non-manufacturing), has a lower momentum in September. The manufacturing index was low at 50.2 and the non-manufacturing index dropped compared to the recent peak of July. On the graph, the trend is flat but consistent with a positive growth. The Fed was right in doing nothing in September.

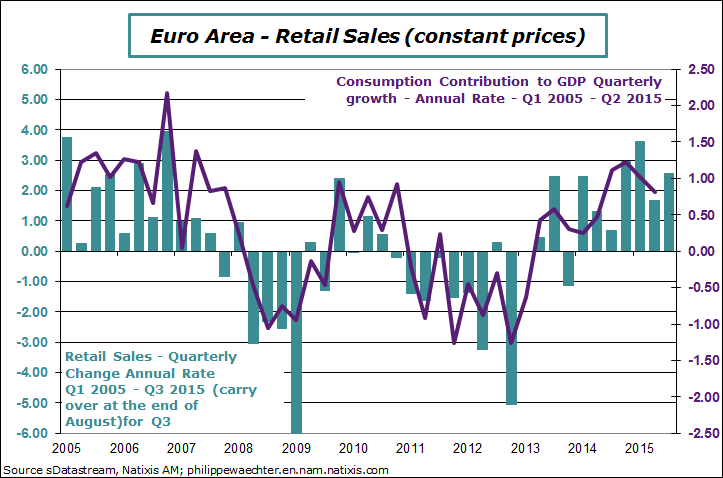

6 – In the Euro Area, retails sales are stronger during the third quarter. The carry over growth for the 3rd quarter at the end of August is at 2.5% (annual rate) versus 1.7% growth during the second quarter. This should convert into a stronger contribution to GDP growth. The geographical detail shows that Portugal, France and Ireland push sales on the upside. Spain’s sales are still at a low-level but the trend is positive.

6 – In the Euro Area, retails sales are stronger during the third quarter. The carry over growth for the 3rd quarter at the end of August is at 2.5% (annual rate) versus 1.7% growth during the second quarter. This should convert into a stronger contribution to GDP growth. The geographical detail shows that Portugal, France and Ireland push sales on the upside. Spain’s sales are still at a low-level but the trend is positive.

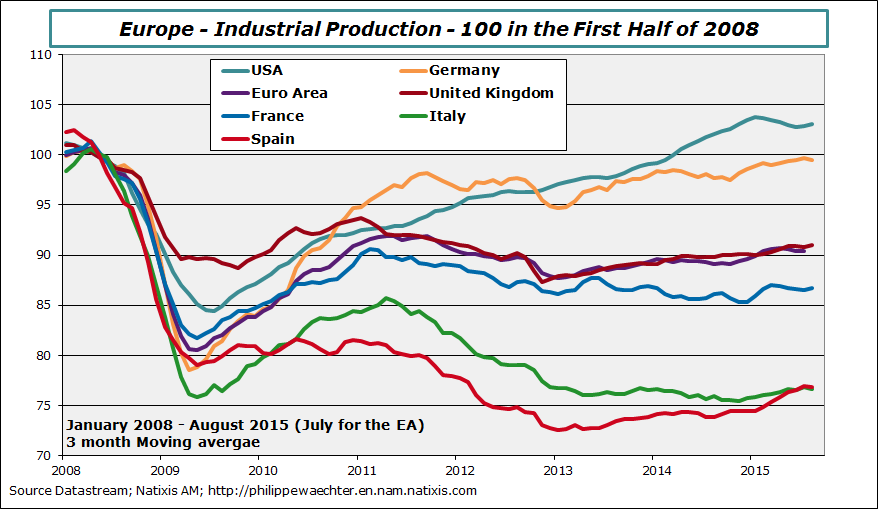

7 – Industrial production indices have been very volatile in Europe during this summer. There was a strong acceleration in August for France and in the United Kingdom, after a drop in July. In Germany and in Spain, indices were down. Carry over growth for the third quarter is positive in Italy at 1.5% (annual rate). This figure must be compared to a 2.1% growth during spring. In France, carry over is 1.1% after -1.7% during the second quarter. In Britain, numbers are +0.9% after +2.7%. In Spain, carry over is a mere 0.6% after +6.5% during spring. In Germany the number is negative for the third quarter after +2% from April to June.

7 – Industrial production indices have been very volatile in Europe during this summer. There was a strong acceleration in August for France and in the United Kingdom, after a drop in July. In Germany and in Spain, indices were down. Carry over growth for the third quarter is positive in Italy at 1.5% (annual rate). This figure must be compared to a 2.1% growth during spring. In France, carry over is 1.1% after -1.7% during the second quarter. In Britain, numbers are +0.9% after +2.7%. In Spain, carry over is a mere 0.6% after +6.5% during spring. In Germany the number is negative for the third quarter after +2% from April to June.

The economic momentum is may be more fragile than expected. That’s what this figures say and it could a source of the prudent ECB behavior.

We see on the graph that in recent months Spain has converged to Italy.

8 – There is good news in the Euro Area. Last week, flows of orders to the German industry were published. The headline number was fragile but the Euro Area subset has a good behavior, specifically on the sub-sector of capital goods. Since last March its improvement is strong and sustained. Its profile is consistent with corporate investment. We can expect a stronger investment dynamics in the months ahead. In fact, internal demand follows currently a higher trajectory (see retail sales above). Expected demand can be stronger in a foreseeable future as oil price will remain low. This is a source for an improvement in companies’ investment.

8 – There is good news in the Euro Area. Last week, flows of orders to the German industry were published. The headline number was fragile but the Euro Area subset has a good behavior, specifically on the sub-sector of capital goods. Since last March its improvement is strong and sustained. Its profile is consistent with corporate investment. We can expect a stronger investment dynamics in the months ahead. In fact, internal demand follows currently a higher trajectory (see retail sales above). Expected demand can be stronger in a foreseeable future as oil price will remain low. This is a source for an improvement in companies’ investment.

In other words, internal demand (households’ expenditures + investment) could be the source of a higher growth momentum in 2016 in the Euro Area. This will not be a catalyst for an ECB move. The Euro Area central banker has still a lot of time.

The German exports ‘ drop in August is not yet an issue of concern.

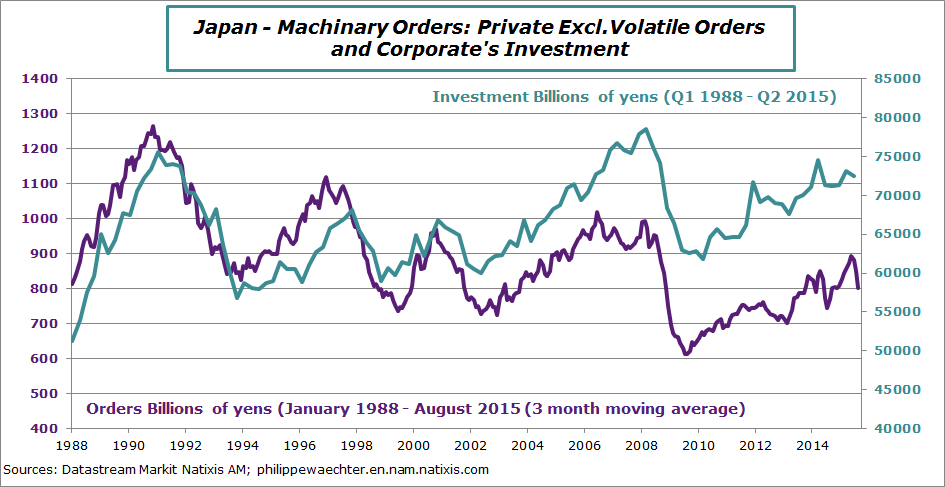

9 – In Japan, capital goods orders have dropped dramatically since May. It is down by -16% since May’s peak and the carry-over growth for the third quarter at the end of August is -40% at annual rate. It was up by 12% during spring. We expect a drop in companies’ investment in the second part of the year. We think that the Bank of Japan is still too optimistic in its perception of the economic outlook

9 – In Japan, capital goods orders have dropped dramatically since May. It is down by -16% since May’s peak and the carry-over growth for the third quarter at the end of August is -40% at annual rate. It was up by 12% during spring. We expect a drop in companies’ investment in the second part of the year. We think that the Bank of Japan is still too optimistic in its perception of the economic outlook

10 – Next week we will have the first surveys for the month of October.

10 – Next week we will have the first surveys for the month of October.

On Tuesday the ZEW will give a first highlight in Germany and on Thursday the Fed of New York and of Philadelphia will do the same for the US. Next Friday the industrial production for the US in September will be announced and on Thursday it is the production index for August in the Euro Area that will be published.

Wednesday, retail sales will be announced in the US. It will give us a better perception of the third quarter momentum on consumption. In the United Kingdom, employment figures for August (employment) and September (wages) will be published (Thursday).

In China, the trade balance will be announced on Tuesday and the inflation rate on Wednesday.

Inflation rate in the Euro Area (Friday), in France (Wednesday), in Germany (Tuesday), in Spain (Wednesday), in the UK (Tuesday) and in the US (Thursday) will be announced for September.

Have a good week