Published in French on October the 26th – Data expected this week but already published are briefly discussed.

8 points to keep in mind this week to highlight the macroeconomic momentum

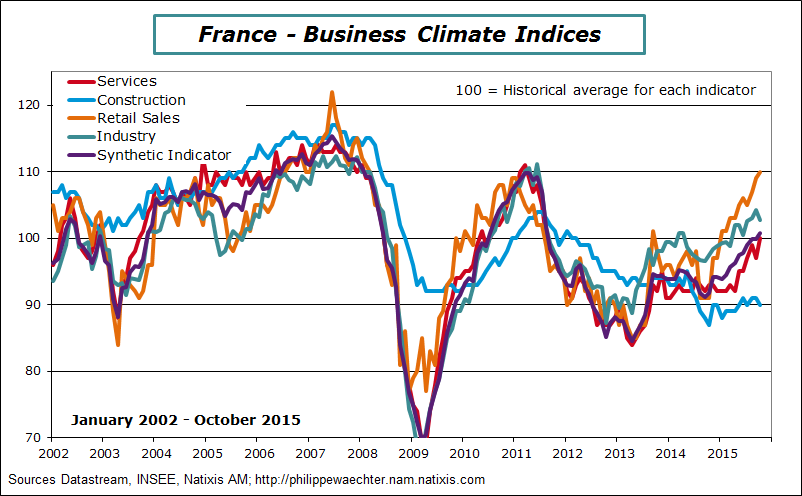

1 – The improvement of the French economy is the real good news

The business climate index, published by INSEE the French Statistical Institute, is above its historical average for the first time since August 2011.

It shows how deep and persistent was the negative shock that has hit the French economy since this period. Looking at the different sectors, building construction is the only one being still on the weak side. Services, Industry and retail trade contribute positively to growth.

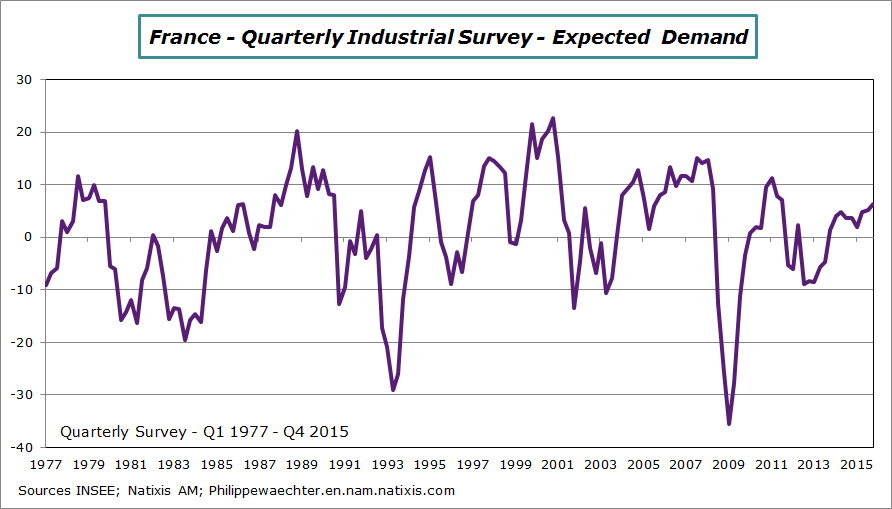

For the French economy we also notice in the INSEE quarterly survey that expected demand is improving rapidly. Companies in the industrial sector anticipate a stronger demand in the near future. This is important to understand that, with this improvement, the probability of a corporate investment recovery in 2016 is now high. Expected demand is the major trigger for investment (see here this paper form La Banque de France)

For the French economy we also notice in the INSEE quarterly survey that expected demand is improving rapidly. Companies in the industrial sector anticipate a stronger demand in the near future. This is important to understand that, with this improvement, the probability of a corporate investment recovery in 2016 is now high. Expected demand is the major trigger for investment (see here this paper form La Banque de France)

This new momentum associated with a trajectory of low oil price and low-interest rates for long will help the French economy to converge to a more robust and attractive profile.

Moreover incentives to invest in France and in Europe are stronger because emerging economies follow a low growth trajectory.

2 – The Markit survey for the Eurozone has also a positive message on the economic outlook in October. The synthetic index is above the corridor seen since last February. This latter was consistent with a 1.5% GDP growth; it could be the start of a higher profile. Published with the Euro index, the French and the German indices are also stronger in October.

2 – The Markit survey for the Eurozone has also a positive message on the economic outlook in October. The synthetic index is above the corridor seen since last February. This latter was consistent with a 1.5% GDP growth; it could be the start of a higher profile. Published with the Euro index, the French and the German indices are also stronger in October.

New orders and employment indices are robust in October. But the synthetic index is supported by the service index which is higher in October (53.2 vs 52.6 in September) whereas the manufacturing index remained at the same level that in September (52).

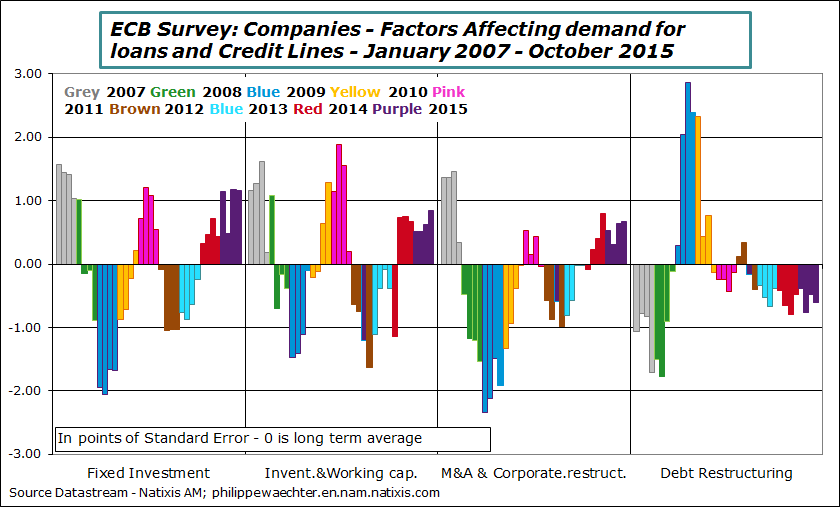

3 – The stronger profile of the Euro Area economy can also be seen in the ECB survey on bank lending. Demand for credit is on the upside specifically for the Small and Medium Business.

3 – The stronger profile of the Euro Area economy can also be seen in the ECB survey on bank lending. Demand for credit is on the upside specifically for the Small and Medium Business.

We can notice on the chart that the companies’ demand for credits is focused on investment and on inventories and working capital. These two items are improving rapidly. It shows short-term momentum is stronger and that companies are ready for stronger commitments in the future. That’s a good combination.

4 – Looking at the world trade dynamics there are still reasons to be on the optimistic side for the Eurozone. World trade in August is following a poor path. It’s increasing by 0.9% on a year after 1.3% in July and 3.4% in June

4 – Looking at the world trade dynamics there are still reasons to be on the optimistic side for the Eurozone. World trade in August is following a poor path. It’s increasing by 0.9% on a year after 1.3% in July and 3.4% in June

Nonetheless the Euro Area has the stronger contribution to the world trade growth. The world economy doesn’t follow a strong trajectory but the Euro Area now has a stronger contribution that shows the Euro recovery. This is a way to start imaging a stronger business cycle in 2016.

Nonetheless the Euro Area has the stronger contribution to the world trade growth. The world economy doesn’t follow a strong trajectory but the Euro Area now has a stronger contribution that shows the Euro recovery. This is a way to start imaging a stronger business cycle in 2016.

5 – The ECB is going this way. An extension of the Quantitative Easing Operation will probably be announced at its next meeting on December the 3rd. This strategy is just to be a support for the recovery by avoiding some kind of volatility in investors and companies’ expectations. To get a stronger investment momentum there is a need for a more stable environment. That’s what the ECB is currently doing and will continue to do with the extension of the QE.

5 – The ECB is going this way. An extension of the Quantitative Easing Operation will probably be announced at its next meeting on December the 3rd. This strategy is just to be a support for the recovery by avoiding some kind of volatility in investors and companies’ expectations. To get a stronger investment momentum there is a need for a more stable environment. That’s what the ECB is currently doing and will continue to do with the extension of the QE.

The ECB strategy is consistent with the Fed’s behavior; they both prefer acting a little too late than too early

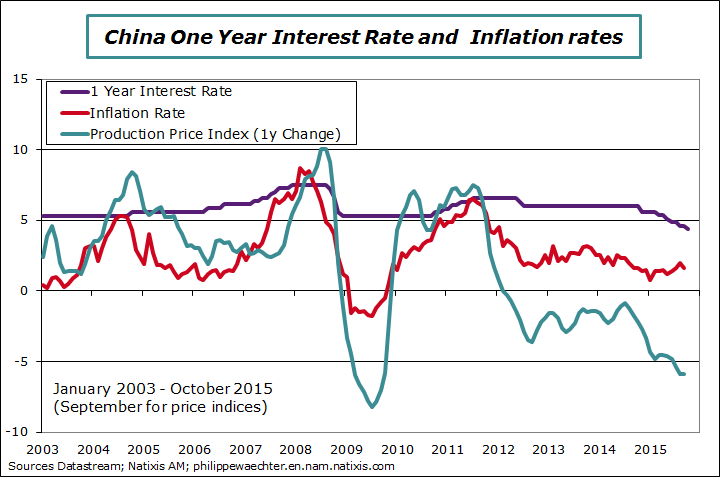

6 – In China the central bank has reduced its interest rates by 25 bp at 4.35% for the one year lending rate and to 1.5% fort the one year deposit rate. The Reserve Requirement Rate was also down by 50bp at 17%.

China is reducing the constraints on growth whereas the economic activity falters. Nevertheless, China is in a huge adjustment process from an industrial led growth economy to a service led growth economy. This will take time and GDP growth will trend downward as services productivity is lower. So the change in monetary policy can help in the very short-term, specifically on land and real estate sectors.

But a simple calculation shows that real interest rate for companies is close to 10 % (interest rate less producer price change) which is way above the GDP growth trend. There is room for lower rates in a deflationary context.

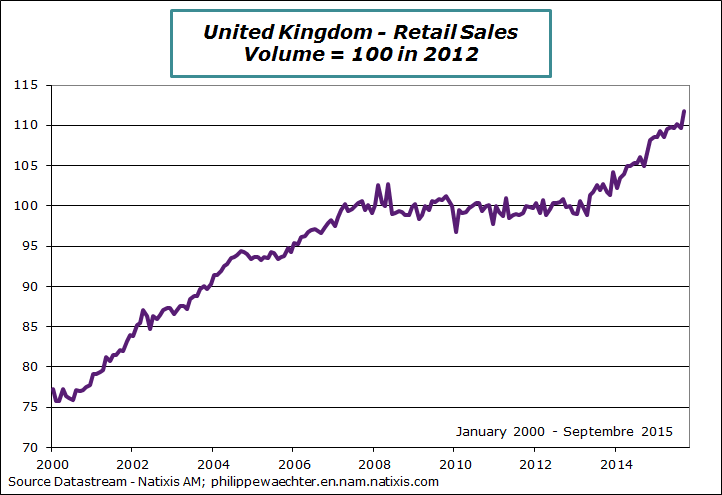

7 – In September, retail sales have been very strong in the United Kingdom. They have increased more rapidly than during spring. It will be a support for GDP growth number which will be publish on Tuesday

7 – In September, retail sales have been very strong in the United Kingdom. They have increased more rapidly than during spring. It will be a support for GDP growth number which will be publish on Tuesday

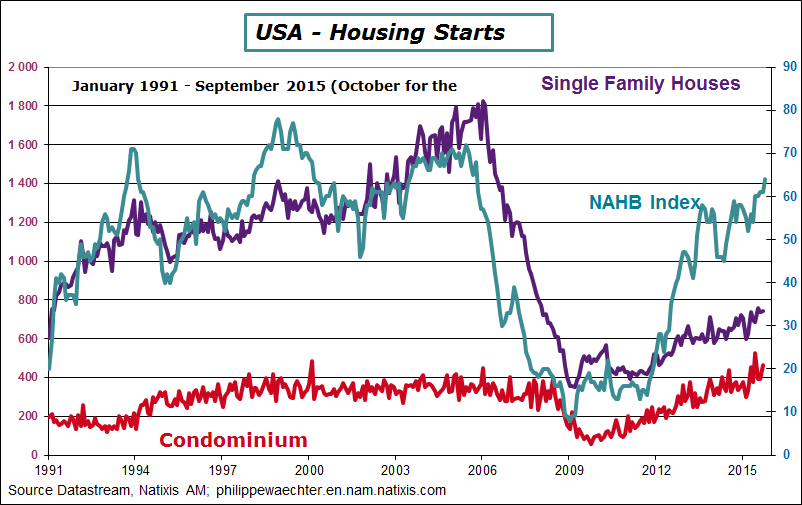

8 – The real estate sector has been stronger during fall. The NAHB index which represents activity for home builders is at its highest since October 2005 and existing home sales are growing rapidly. This latter point is important as it reflects the only wealth effect that really works. Strong sales mean higher price and higher value for everyone house. This leads to more positive expectations for the future. It’s a support for households’ expenditures. It is a much stronger effect than the wealth effect linked with financial assets. It reflects the fact that the real estate is an issue for everyone.

8 – The real estate sector has been stronger during fall. The NAHB index which represents activity for home builders is at its highest since October 2005 and existing home sales are growing rapidly. This latter point is important as it reflects the only wealth effect that really works. Strong sales mean higher price and higher value for everyone house. This leads to more positive expectations for the future. It’s a support for households’ expenditures. It is a much stronger effect than the wealth effect linked with financial assets. It reflects the fact that the real estate is an issue for everyone.

For the week to come the most important point is the Fed’s meeting on October the 27 and 28. Looking at macroeconomic data there is no reason for the US central Bank to change its strategy. There are no tensions in the US economy that could justify a change in interest rates. I’m not sure that the situation will be different in December. I don’t expect a change in monetary policy this year. No press conference is scheduled

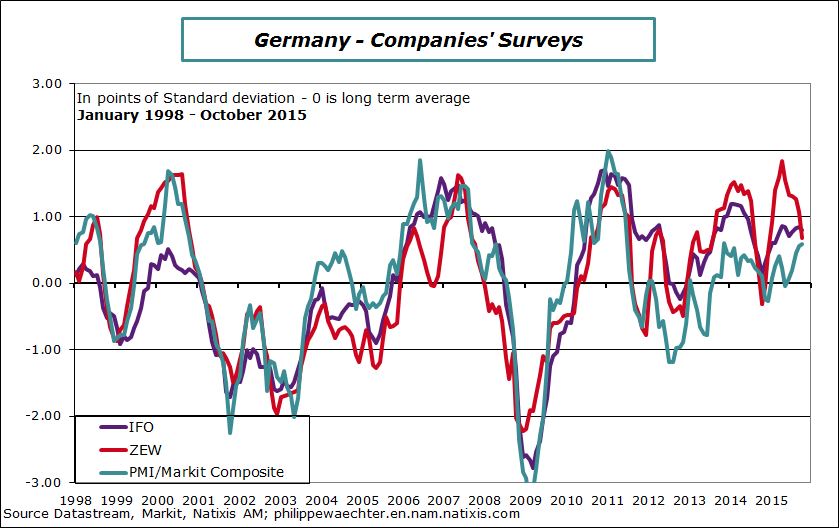

The IFO index has been published on Monday in Germany. It’s a little lower but the German economy is still doing well as it is shown on the graph. The 3 indices are still way above their average. Adjustment on the ZEW reflects correction after an excess.

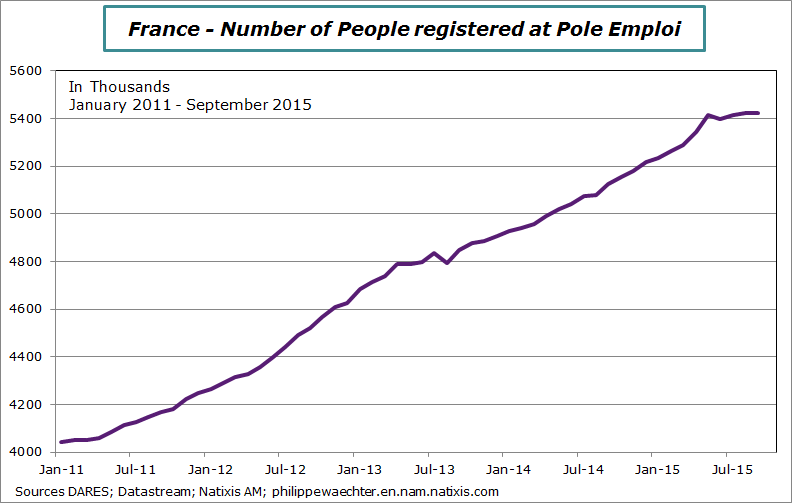

Jobseekers’ number for September in France was published on Monday. There is a real change in trend and we can say that the expected improvement on the French economy will provoke a U-turn on the labor market

Jobseekers’ number for September in France was published on Monday. There is a real change in trend and we can say that the expected improvement on the French economy will provoke a U-turn on the labor market

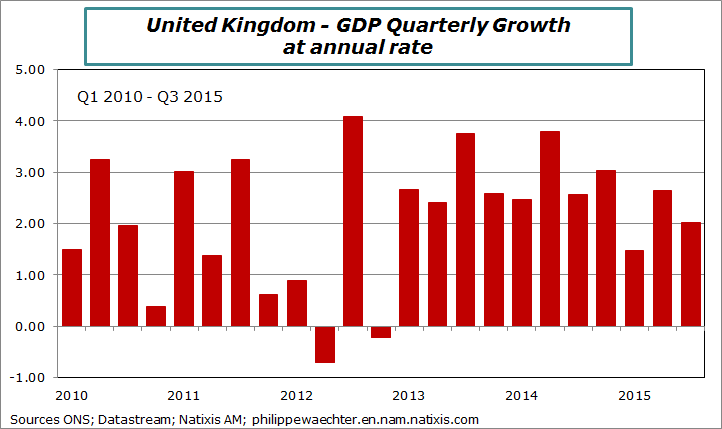

In the United Kingdom the GDP growth number for the third quarter was published at 0.5% (2% at annual rate). it is below Q2 growth (0.7% and 2.6% at annual rate)) and below expectations (0.6% and 2.4% at annual rate)

In the United Kingdom the GDP growth number for the third quarter was published at 0.5% (2% at annual rate). it is below Q2 growth (0.7% and 2.6% at annual rate)) and below expectations (0.6% and 2.4% at annual rate)

GDP growth numbers for the third quarter will be published in the US (Thursday) and in Spain (Friday). The US growth figure will probably be way below what was seen in the second quarter (3.9%).

GDP growth numbers for the third quarter will be published in the US (Thursday) and in Spain (Friday). The US growth figure will probably be way below what was seen in the second quarter (3.9%).

On Wednesday, durable goods orders in the US will give a good preview on corporate investment.

In Japan industrial production figures for September will be published on Wednesday and employment and retail sales for September will be available on Thursday. This will provide more accurate profile of the Japanese, including the likelihood of a recession.

In Japan industrial production figures for September will be published on Wednesday and employment and retail sales for September will be available on Thursday. This will provide more accurate profile of the Japanese, including the likelihood of a recession.

Friday we will have for the Eurozone advanced estimate for the inflation rate in October and the unemployment rate for September. It will also be spending by French households in September.

Have a good week everybody