The main issue this week was the US employment figure as it may change the Fed’s mind on monetary policy. Nevertheless, employment is not the only aspect to mention to catch the US economy momentum. Another important issue, this week, is the rapid and deep drop of German industrial orders from outside the Euro Area. It’s a source of concern for the global investment dynamics. The last important point is the non-null probability of a rate lift-off at the Bank of England in 2016. Mark Carney has mentioned this possibility after the Monetary Policy Committee Meeting of the Bank. It’s not the first time that the BoE and Carney take this kind of commitment.

Eight points this week to follow the macroeconomic environment

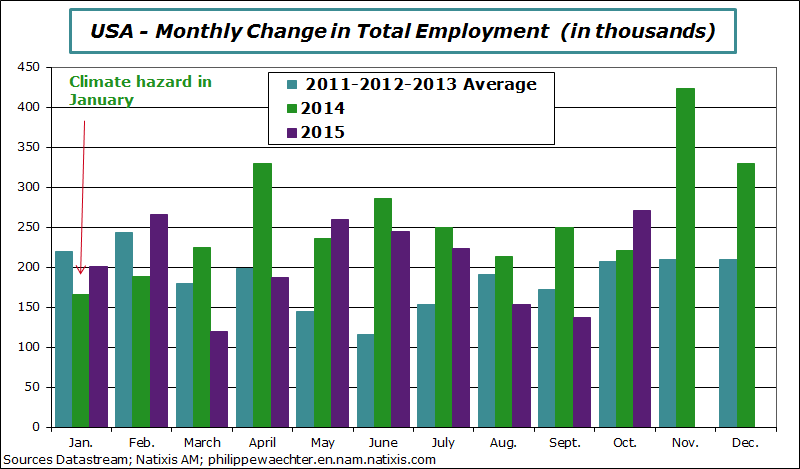

1 – There was impatience to get the number of jobs creation in October in the US as it could be a trigger for a Fed’s rate move at its December meeting.

The number was strong at 271 000, way above expectations at 185 000. Nevertheless, the employment rate was almost unchanged for all classes of age and was unchanged for the 25-55 years of age. In other words, there were no supplementary pressures on the labor market even with employment surprising on the upside.

This figure comes after August and September during which the number of jobs creation was low. As a consequence, the average number of new jobs in the last 3 months is below the average of the 3 previous months: +187 000 in August, September and October versus 243 000 from May to July.

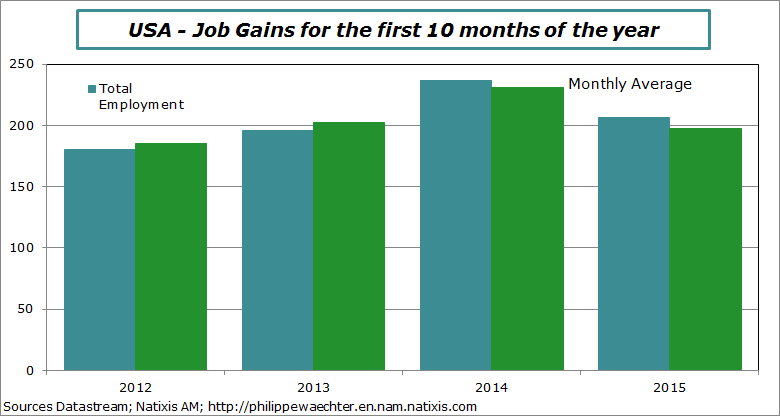

For the first ten months of the year, 2015 is weaker than 2014 with 206 000 jobs each month versus 236 000 last year.

For the first ten months of the year, 2015 is weaker than 2014 with 206 000 jobs each month versus 236 000 last year.

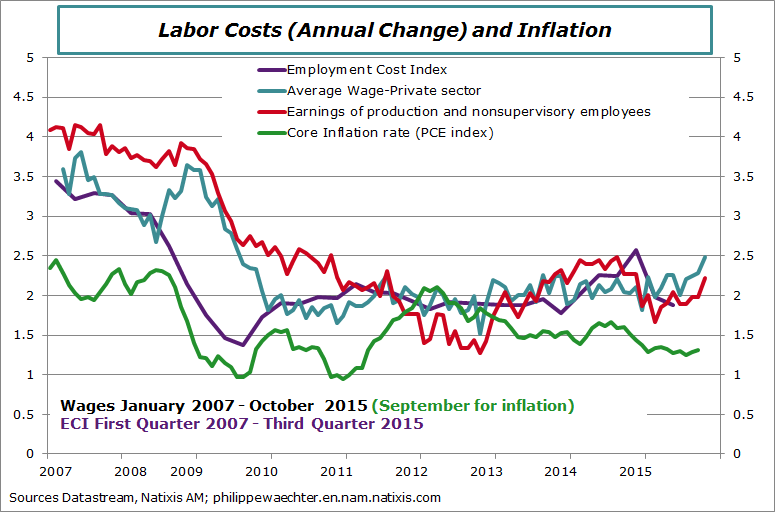

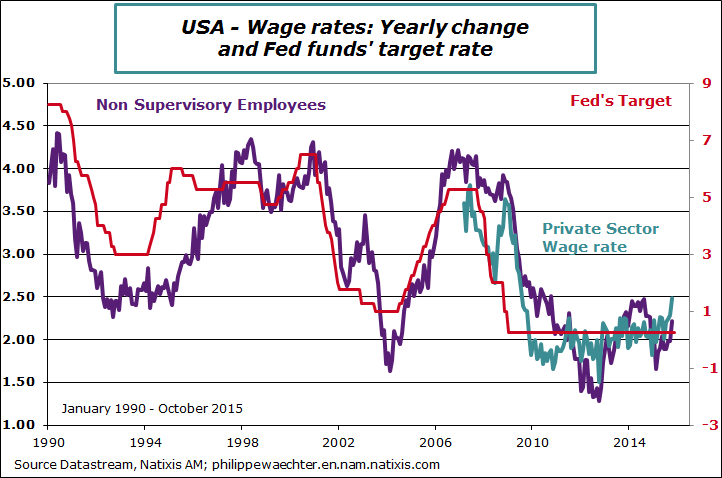

The main change in the October’s report was a surge in the wage rate growth. The average wage rate for the private sector is up by 2.5% way above the corridor of 1.9-2.2% seen since 2012.

The main change in the October’s report was a surge in the wage rate growth. The average wage rate for the private sector is up by 2.5% way above the corridor of 1.9-2.2% seen since 2012.

The employment report is robust in October: the question then is to know if the improvement is a change in trend or a simple catch up? If it’s a new trend, then the US central bank will be credible to act but if it is just a catch up incentives to act will be low.

The employment report is robust in October: the question then is to know if the improvement is a change in trend or a simple catch up? If it’s a new trend, then the US central bank will be credible to act but if it is just a catch up incentives to act will be low.

A single figure, as was the labor report, is nevertheless not sufficient to make the decision even if it is robust. There is a need for a confirmation at the beginning of December for the November labor report.

For a more complete report on the US job report see here

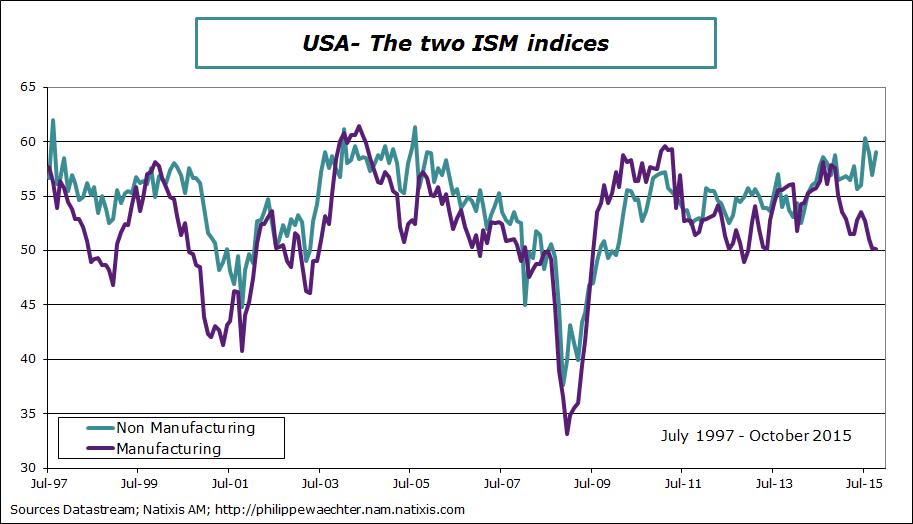

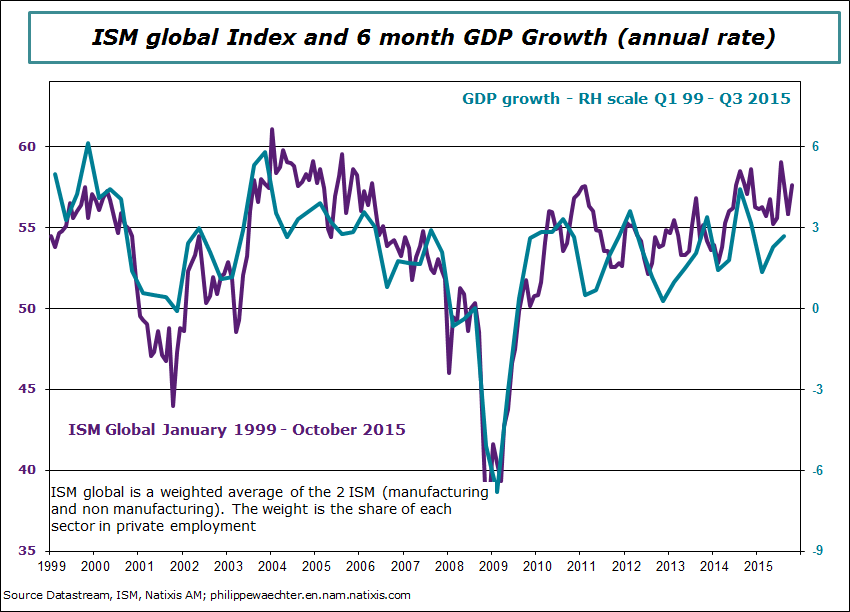

2 – Surveys on the US activity have very different profiles. The ISM for the manufacturing sector is trending downward with an index at only 50.1 in October. At the same time, the non-manufacturing ISM survey has an index close to its recent high at 59.05. The non-manufacturing series is available since July 1997. For the whole period, such a divergence between the two indices has never been seen. What is worrisome is the fact that usually, fluctuations on the manufacturing survey are prior those on the non-manufacturing. This could converge to weakness in the US economy

If we combine the two surveys in the ISM global, this latter is back to a high level, consistent with a sustained GDP growth profile.

If we combine the two surveys in the ISM global, this latter is back to a high level, consistent with a sustained GDP growth profile.

The US economy is supported by the sector of the services but with a low momentum on the manufacturing side. I have already mentioned this issue after looking at the production capacity utilization rate (see here)

3 – There are still uncertainties on the monetary policy profile after December meeting. Is it a change in trend or a catch up? We need other data on the labor market but also on economic activity and consumption in order to have a clear picture. The divergence between the two ISM is a puzzle that is not solved yet. The Federal Reserve must have a clear conclusion on this divergence before taking a decision.

3 – There are still uncertainties on the monetary policy profile after December meeting. Is it a change in trend or a catch up? We need other data on the labor market but also on economic activity and consumption in order to have a clear picture. The divergence between the two ISM is a puzzle that is not solved yet. The Federal Reserve must have a clear conclusion on this divergence before taking a decision.

If the job number was repeated in November, the Fed would be able to fulfil its commitment to change its strategy on the upside in 2015. But this would not tell something for 2016 as we know that Janet Yellen doesn’t have in mind a rapid increase of the Fed’s rate.

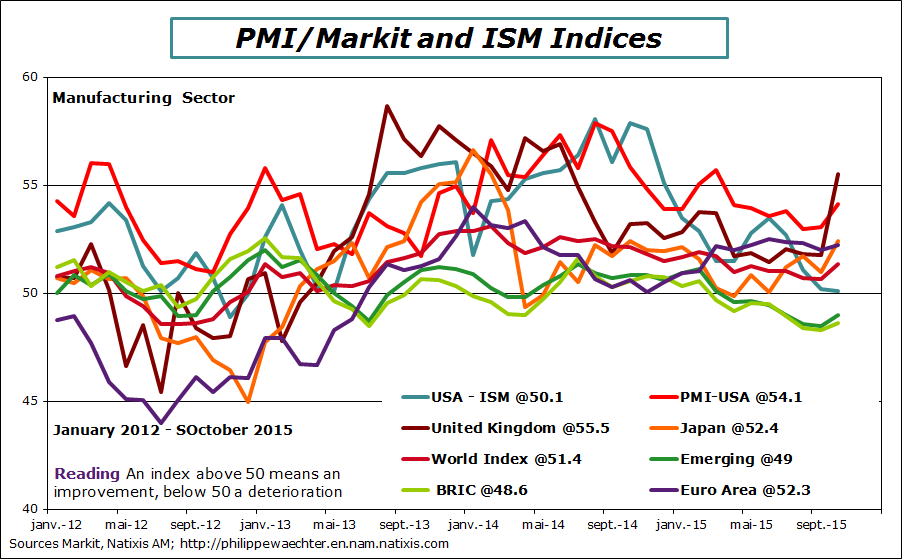

4 – Surveys by Markit and ISM for the manufacturing sector are a bit stronger in October. The world index is a bit higher at 51.4 versus 50.7 in September. This reflects an improvement of the US Markit survey and a less negative index in China. Surveys in Japan, the Euro Area and the United Kingdom are also supportive. The ISM index for the manufacturing sector is following an opposite trend at just 50.1. That’s puzzling.

4 – Surveys by Markit and ISM for the manufacturing sector are a bit stronger in October. The world index is a bit higher at 51.4 versus 50.7 in September. This reflects an improvement of the US Markit survey and a less negative index in China. Surveys in Japan, the Euro Area and the United Kingdom are also supportive. The ISM index for the manufacturing sector is following an opposite trend at just 50.1. That’s puzzling.

We notice that the UK index is improving rapidly while the CBI index was down. Usually the two indices have consistent profiles. There is something to understand better

Emerging countries indices are still low, below the threshold of 50. Russia is converging to 50 from the bottom, India is still above 50 but following a slow pace and Brazil is at its lowest level since March 2009. Recession in Brazil is far from being over.

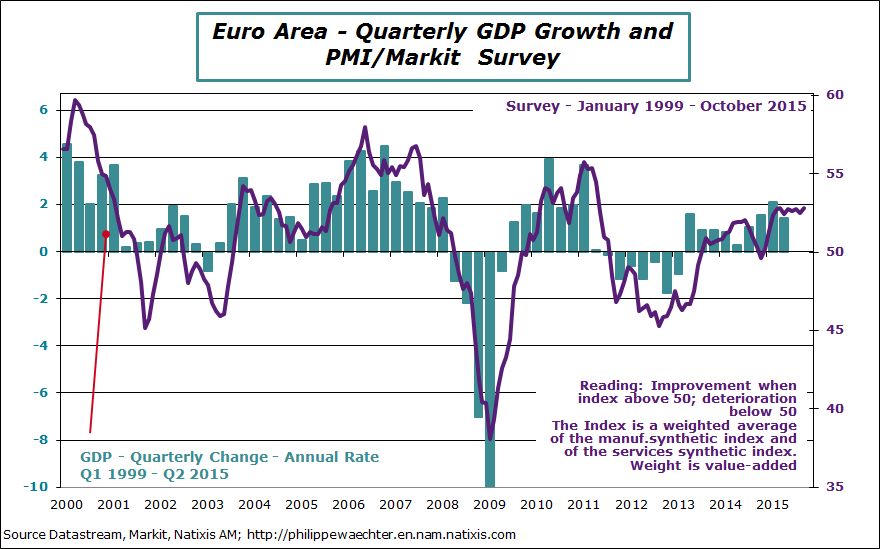

5 – In the Euro Area, the Markit index for the whole economy is a bit higher in October at 52.8 versus 52.5 in September. Still consistent with a 1.5% GDP growth but doesn’t show an acceleration. The New Orders to Inventories is sliding a bit at 1.07 versus 1.1 last August. Industrial production momentum will not accelerate in the coming months.

5 – In the Euro Area, the Markit index for the whole economy is a bit higher in October at 52.8 versus 52.5 in September. Still consistent with a 1.5% GDP growth but doesn’t show an acceleration. The New Orders to Inventories is sliding a bit at 1.07 versus 1.1 last August. Industrial production momentum will not accelerate in the coming months.

In France, the global Markit index is up by 1 point to 51.7 in October. The New Orders to Inventories ratio is marginally higher at 1.04 versus 1.02 in September. It’s better but not creating a strong autonomous dynamics.

In France, the global Markit index is up by 1 point to 51.7 in October. The New Orders to Inventories ratio is marginally higher at 1.04 versus 1.02 in September. It’s better but not creating a strong autonomous dynamics.

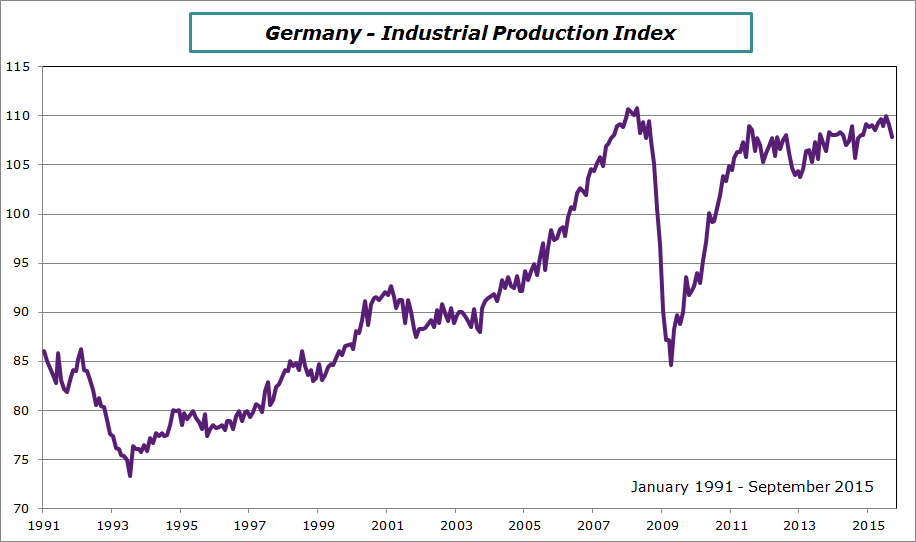

6 – In Germany, the industrial production index was down by -1.2% in September. During the third quarter the index has fallen by 1.3% at annual rate.

6 – In Germany, the industrial production index was down by -1.2% in September. During the third quarter the index has fallen by 1.3% at annual rate.

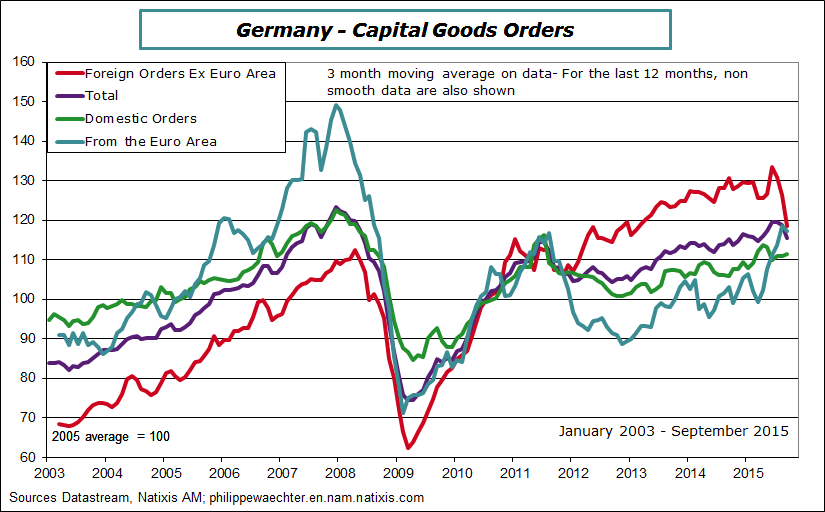

Industrial new orders follow a weak momentum. For the last three months compared to the previous three months there are down by -10.8% at annual rate. The rest of the word ex euro area has a very negative contribution. Orders from the rest of the world are down by -30.2% for the last three months. Capital goods orders are decreasing at a very rapid pace at -38% for the third quarter compared to the second. This means that investment in the rest of the world (ex Euro Area) is following a very weak trajectory. This is really bad news as potential GDP will not be reinforced. Germany is also harmed by the weakness seen recently in Asia and mainly in China.

Industrial new orders follow a weak momentum. For the last three months compared to the previous three months there are down by -10.8% at annual rate. The rest of the word ex euro area has a very negative contribution. Orders from the rest of the world are down by -30.2% for the last three months. Capital goods orders are decreasing at a very rapid pace at -38% for the third quarter compared to the second. This means that investment in the rest of the world (ex Euro Area) is following a very weak trajectory. This is really bad news as potential GDP will not be reinforced. Germany is also harmed by the weakness seen recently in Asia and mainly in China.

At the same time, capital goods orders follow a stronger trajectory in the Eurozone during the third quarter: Could be good for investment.

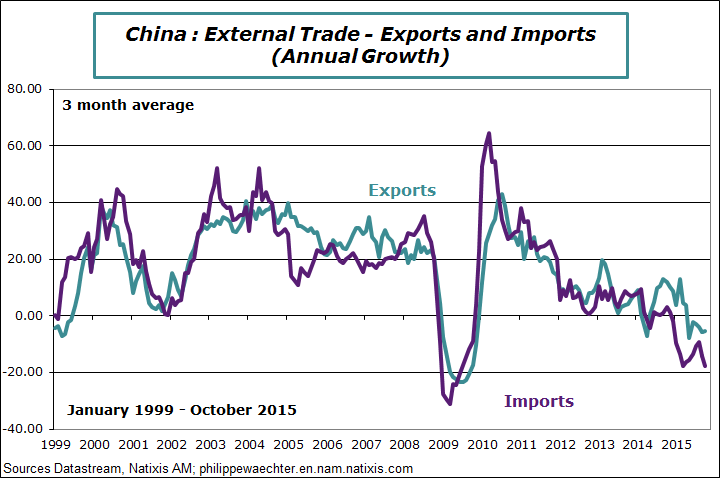

7 – The Chinese trade surplus is skyrocketing. It is at USD 61.6bn in October and at a historical high when accumulated on the last 12 months (USD 593bn)

7 – The Chinese trade surplus is skyrocketing. It is at USD 61.6bn in October and at a historical high when accumulated on the last 12 months (USD 593bn)

This reflects mainly a deep drop in imports but at the same time a very weak momentum in exports. Imports are by -18.8% in October (compared to October 2014) after -20.4% in September (but -17.8% on the last three months compared to the same three months last year). Exports are falling by -6.9% after -3.7 % in September (but -5.3% when comparing the last months to the same three months last year). This large imbalance reflects an excess of saving and the deceleration of investment.

This reflects mainly a deep drop in imports but at the same time a very weak momentum in exports. Imports are by -18.8% in October (compared to October 2014) after -20.4% in September (but -17.8% on the last three months compared to the same three months last year). Exports are falling by -6.9% after -3.7 % in September (but -5.3% when comparing the last months to the same three months last year). This large imbalance reflects an excess of saving and the deceleration of investment.

China perceives the impact it has had for years. It has fed exports from the rest of the world. But now as Chinese dynamics is lower, these countries (especially emerging) lack a source of growth and cannot import as such as they did in the past.

8 – Mark Carney said that the Bank of England interest rates could go up in 2016. It’s not the first commitment of this type from Carney but at each time in the recent past, the Bank was not able to fulfill it. Will it be the same in 2016? It’s a possibility which is associated with a loss of credibility.

For the coming week, the main publication will be GDP growth for the third quarter in the Euro Area. It will be next Friday. The French figure will be out at 0730. We don’t expect acceleration and the number will probably be circa 0.3-0.4%.

The other important publication will be retail sales figures for October in the US. It could highlight the real current momentum after two months in August and September with limited improvement. It will be Friday

In China, after the inflation rate for October (Tuesday) we will have data on retail sales, on investment and on industrial production. It will be on Wednesday

We will have jobs number in the United Kingdom on Wednesday, industrial production in France and Italy (Tuesday) and for the Euro Area on Thursday. The Inflation rate in France and Germany will be available on Thursday

Good week to everyone

This column was published first in French on Monday the 9th