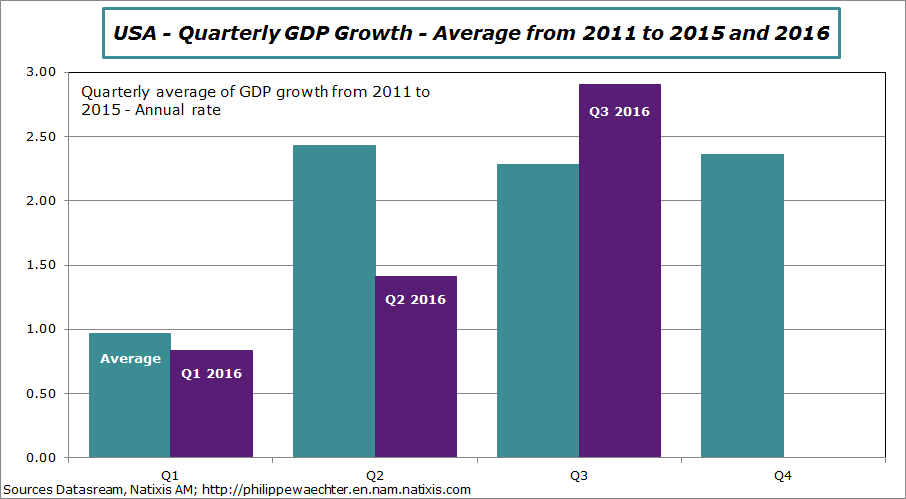

GDP growth was at 2.9% in the third quarter after 1.4% during spring. The carry over growth for 2016 at the end of the third quarter is 1.4%. Growth for the whole year can now be expected at 1.6%.

During the third quarter we’ve seen a catch up that partly compensate the weak figure of the second quarter.

This doesn’t create pressures that could push the Fed to act rapidly. It will do nothing during its next meeting(next week) and we still anticipate a 25bp hike during the December FOMC meeting. The trend in the economy is not strong enough to imagine a rapid pace of increase from the Fed. We think that the Fed will give minimum guidances for what it will do in 2017 in order to limit crazy expectations (remember the beginning of 2016).

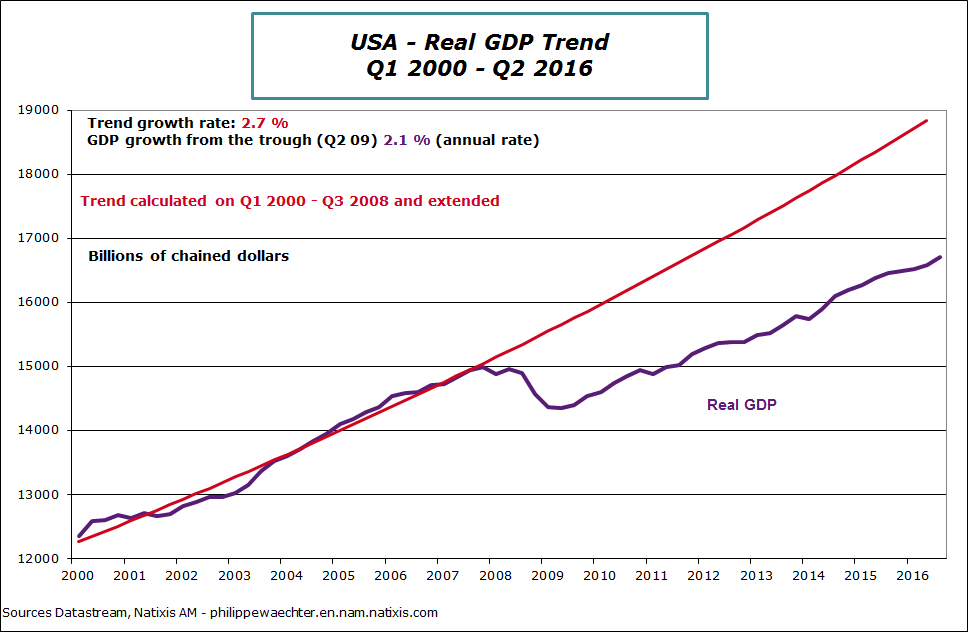

We see on the following graph that the GDP trend is around 2.1% in this cycle which way below what was seen before the crisis. This cycle is the worst since WWII and that’s an important reason not to act too rapidly.

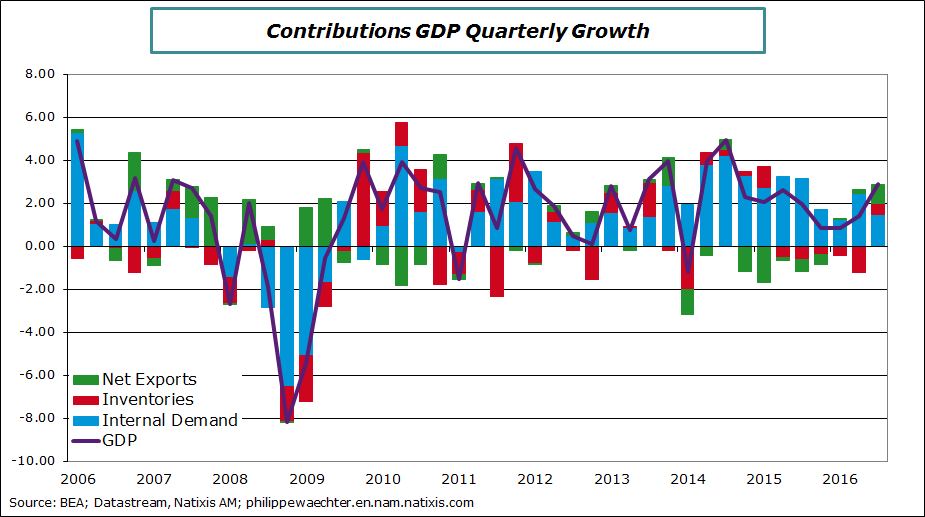

The composition of the GDP is interesting. The graph shows contributions to GDP growth.

We see that internal demand is almost stable and that’s the main source of growth. But we see that this doesn’t reflect in a strong momentum for the GDP. That’s why the increase in investment in infrastructure is interesting. it could create incentives for private productive investments boosting growth. This could help to exit the risk of secular stagnation

.

.