The Fed will decide, with a high probability, to increase its main rate by 25 bp at its meeting today. The US central bank has mentioned so many times this hike that it has to do it. It’s a question of credibility.

What will happen in 2017?

My analysis

Monetary policy in the current cycle is the main support for the private domestic demand in order to boost growth. This has always be the case but the current situation is specific for three reasons

1 – The world trade momentum is not strong enough to create an impulse on growth. In the past, this momentum was strong and the impulse associated with it was important as it helped the economy to converge to a higher profile. This was important for Europe.

2 – The low productivity momentum in the US has not allowed for a strong rebound after the last US recession. Therefore the US growth pace is lower than before and its impact on the world economy is weaker

3 – Fiscal policies are neutral since 2014. This highlights the role of the private domestic demand in the current environment

The private domestic demand profile is not robust in the current business cycle (see graphs in the appendix). Therefore, in order to boost growth, central banks must create incentives for the private sector to spend now rather than later. In other words, the monetary policy stance must limit wealth transfers from the present to the future. That’s the main reason for low interest rates. Central banks fix the short term rate (fed funds in the US or refi in the EA) and are able to intervene on longer maturities. That’s the role of QE in the EA. It’s also the main reason for the Bank of Japan to target the 10 year bond rate at 0%. The point is to reinforce private demand momentum now.

What will change in 2017?

The US private domestic demand will be boosted by the large tax cuts that are in the president-elect program. In that case the monetary policy role will change dramatically. The need for low rates to support the private demand will be reduced due to a more proactive fiscal policy.

The more balanced policy mix will be more efficient.

In the recent past, the Fed’s strategy was twofold

1 – It wanted to regain margin in the management of its monetary policy. The current level was too low in case of a negative shock on the economy. The expected rate hike at today’s meeting reflects this point and not the absolute necessity to reduce pressures on the economy.

2 – Until now, the Fed’s analytical framework was based on the asymmetric impact of the monetary policy. Acting too rapidly was perceived as taking a risk on the growth momentum, acting too late was associated with higher inflation. The Fed thought, rightly, that it was better to act a little too late than a little too early. (see Lael Brainard)

With a proactive fiscal policy, the Fed’s margin will increase and it will be able to increase it’s rate with a different profile than what was expected before. We can expect at least 2 rate’s hike in 2017.

The stronger growth and a higher rate from the Fed mean than the 10 year bond rate could converge to 3%.

During Janet Yellen press conference we will be very attentive to the Fed’s new analysis of the context and what she will say on 2017 new environment.

Appendix

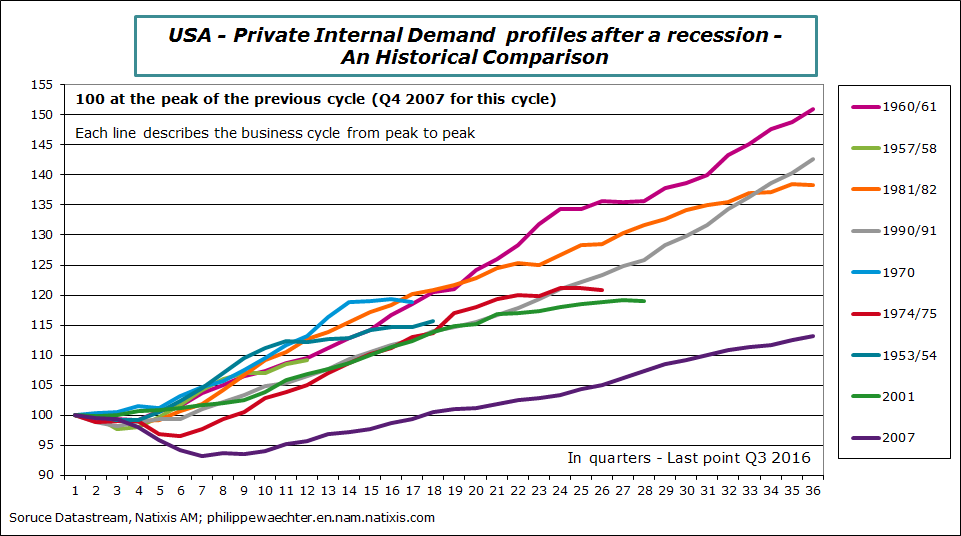

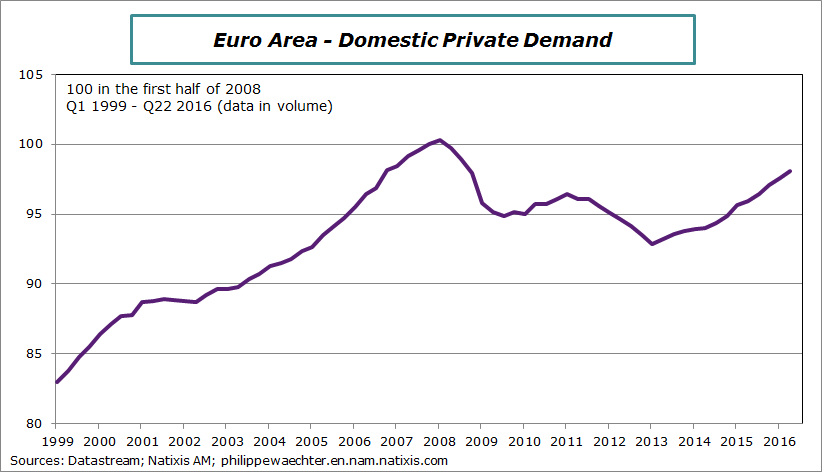

The first graph shows the domestic private demand in the Euro Area. The second graph shows US domestic private demand.

On the Euro Area

The level of the domestic private demand is still, at the end of Q2 2016, below its 2008 level. The trend was on the upside before 2007 but we see a fracture since then. Two reasons for that: the Lehman moment in September 2008 and austerity policies after 2011.

As far as the domestic private demand remains weak the ECB will maintain a very accommodative monetary policy

On the US

Each line on the graph represents the domestic private demand during a cycle since WWII. All the lines have a kind of common trend, except the current cycle. That’s the main reason for a specific strategy from the Fed.