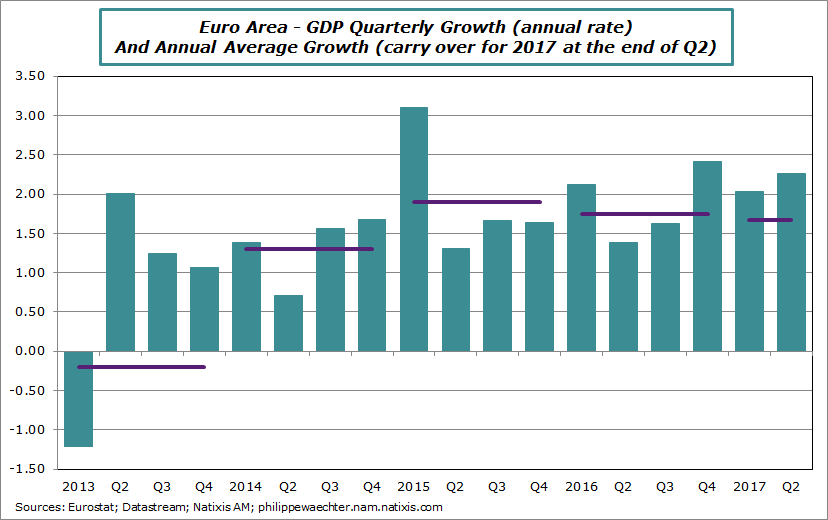

Strong growth during the second quarter

GDP growth was marginally stronger during the second quarter in the Euro Area. It was at 0.56% (2.26% at annual rate) after 0.51% (2.04% AR) during the first three months of this year. The growth profile has been slightly modified with this publication. Formerly, GDP growth for the first quarter was at 0.58%.

Carry over growth for 2017 at the end of the second quarter is 1.7%, close to 2016 average growth. We see on the graph that during the last three quarters growth is stable and close to 2% (at annual rate).

When we look at corporates’ surveys (see below), we can infer that GDP growth could be close to 0.5% (2% at annual rate) during the last two quarters of 2017. In that case the average growth for 2017 could be at 2.1%.

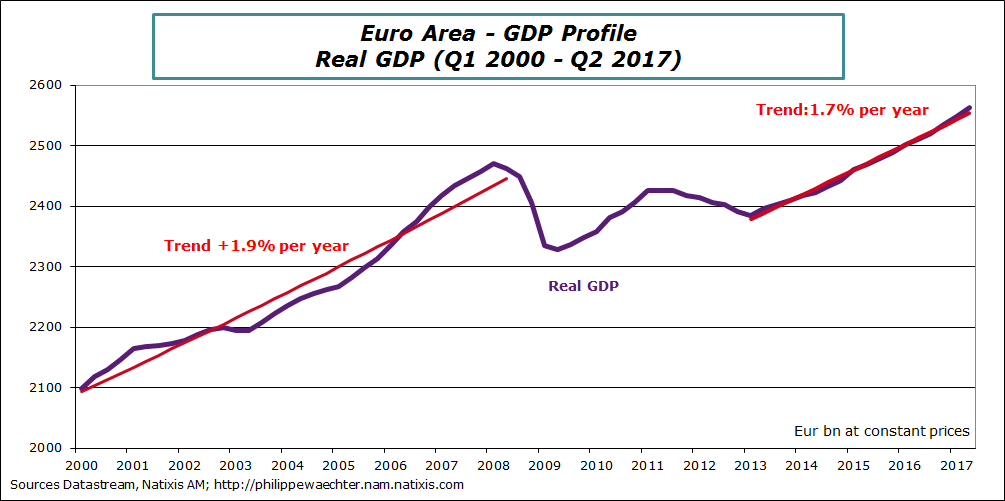

Since the trough of the cycle (Q1 2013) the GDP growth trend is 1.7%. It is just 0.2% below the pre-crisis trend. The bleak period (2009-2012) is now clearly behind us.

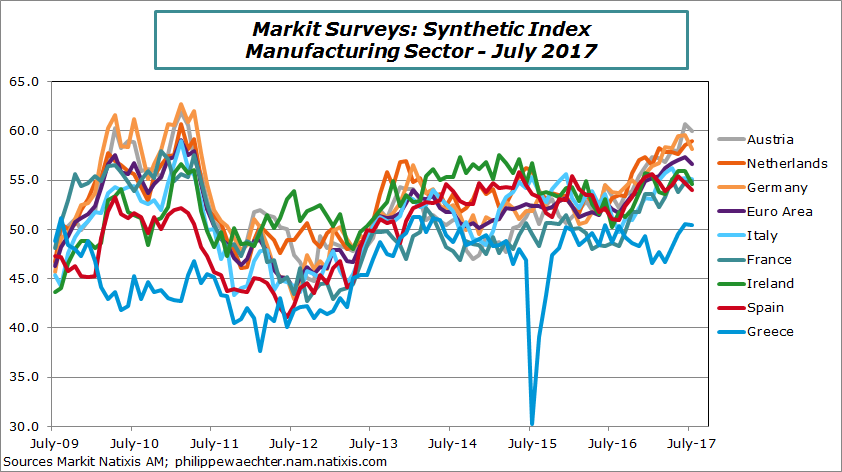

Corporates’ survey – The manufacturing sector is growing rapidly

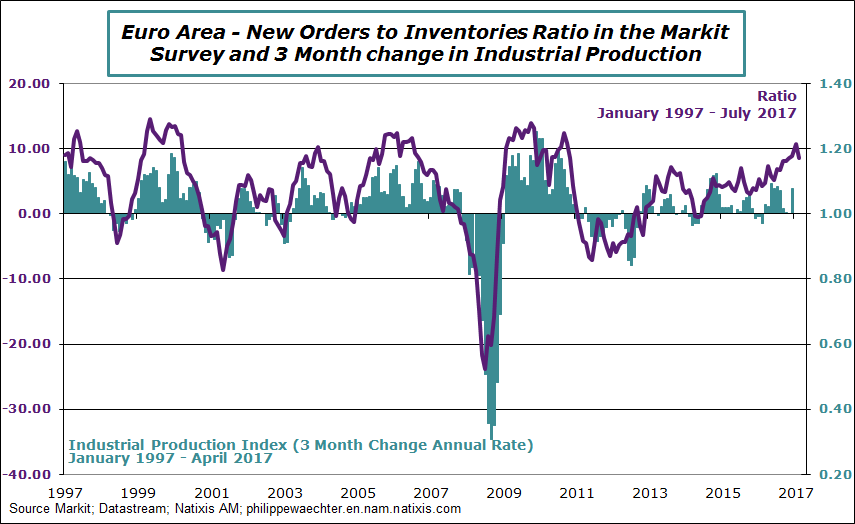

The Markit survey for the Euro Area shows that activity in the manufacturing sector remains robust at the beginning of the third quarter even if the index level is marginally below its June level.

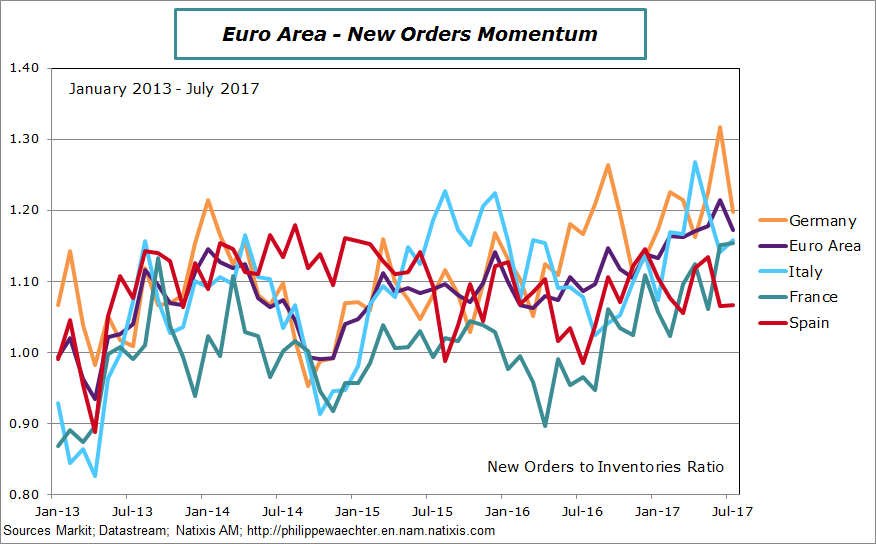

The graph shows that every country follows a strong momentum, even Greece for which the index is above 50 for the second month in a row.

The new orders dynamics is marginally weaker than in June but this is due to Germany. In June its index was abnormally strong and July is just a normalization. That’s what we see from the graph below that shows the new orders to inventories ratio. For Germany the June acceleration is associated with domestic demand not foreign demand even if this latter is marginally weaker than in May

For the other three large countries of the Eurozone, the situation is steady in July.

We are still on a stronger momentum scenario for the manufacturing sector as it can be seen on this graph.

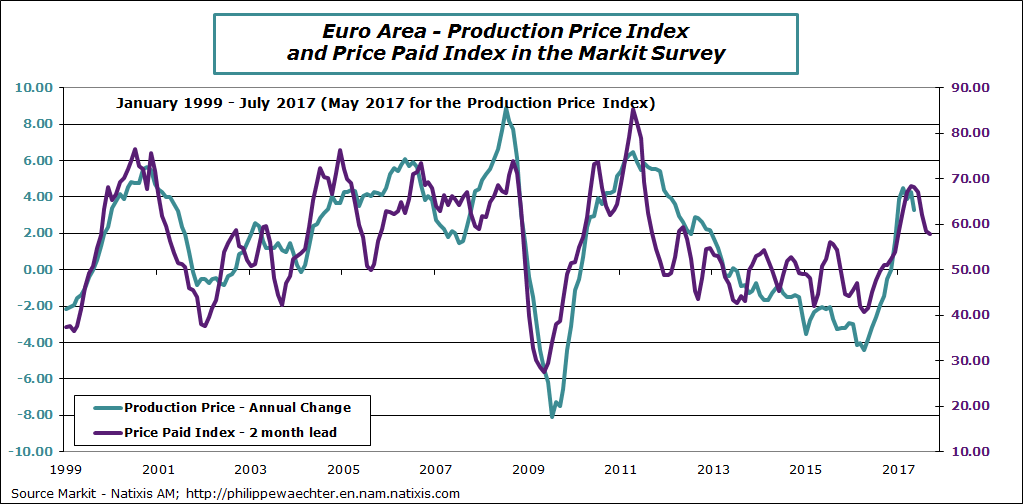

Nominal pressures in the Markit survey are lower in July. It will lead to lower inflation rate at the production level. It’s an incentive for the ECB to maintain the accommodative stance of its monetary policy