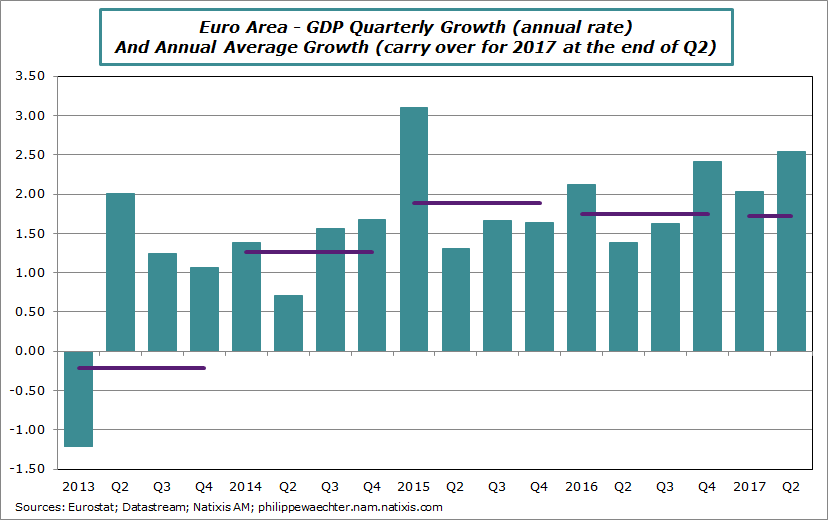

Growth has been robust since the beginning of 2017. In the second quarter, the economic activity was up by 2.5% after 2% during the first quarter and 2.4% in the last three months of 2016 (annual rates). Compared to the second quarter of 2016 the GDP level is 2.15% higher and the carry over growth for 2017 at the end of the second quarter is 1.7% (in other words, if growth is 0% in the third and the fourth quarters than the average growth for 2017 will be the same than in 2016). The graph shows this with a strong acceleration during the last three quarters.

Corporates surveys suggest that the growth momentum is strong so the Euro Area GDP growth will be above 2% on average for 2017 (2.1% for Natixis AM)

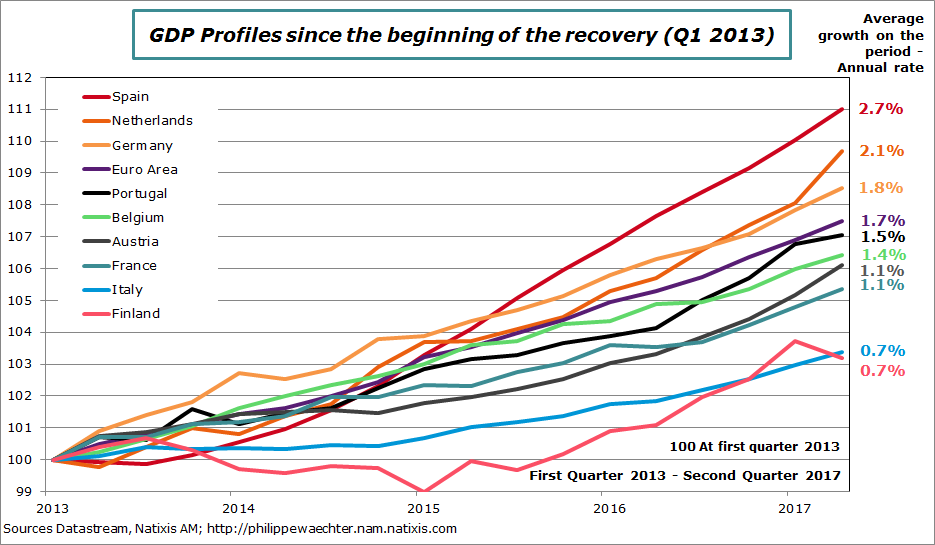

This rapid growth improvement can be seen in every country except in Finland. That’s what shows the table below.

Spain, Austria, Portugal and the Netherlands have had a very strong growth dynamics during the first half of 2017. Their carry over for 2017 is strong and is now above the figure for the Euro Area. The German economy is doing a little bit better than the Euro Area while France lags it even if recent data are stronger. The carry over for France is just 1.4% way below the Euro Area average of 1.7%. The Italian profile is steeper than before but still weak. The catch up is limited as Italy has had a deep and prolonged recession that has reduced dramatically its potential.

The domestic demand momentum explains this growth improvement. Uncertainty associated to economic policies is now low, much lower than during the period of austerity. Households and companies now react to their own constraints and no longer to uncertain expectations on economic policies (specifically on fiscal policies). This reduction of the uncertainty has led to a catch up in employment, consumption and investment. The global context is also very supportive: the world trade recovery is a strong impulse for growth, the oil price is low and stable and interest rates are expected to remain low for an extended period.

Since the beginning of 2013, start of the recovery, GDP profiles have been very heterogenous in the Euro Area. This heterogeneity is a clear incentive for very accommodative economic policies notably from the ECB. This accommodative stance will reinforce the virtuous dynamics of this recovery. This will be key for France and Italy for which the trajectory is still weak.

Since 2013, Finland and Italy have a 0.7% growth on average versus 2.7% for Spain and 1.7% for the Euro Area. With 1.1% France is lagging the rest of Europe. Macron’s task is to create conditions for a more robust trajectory.