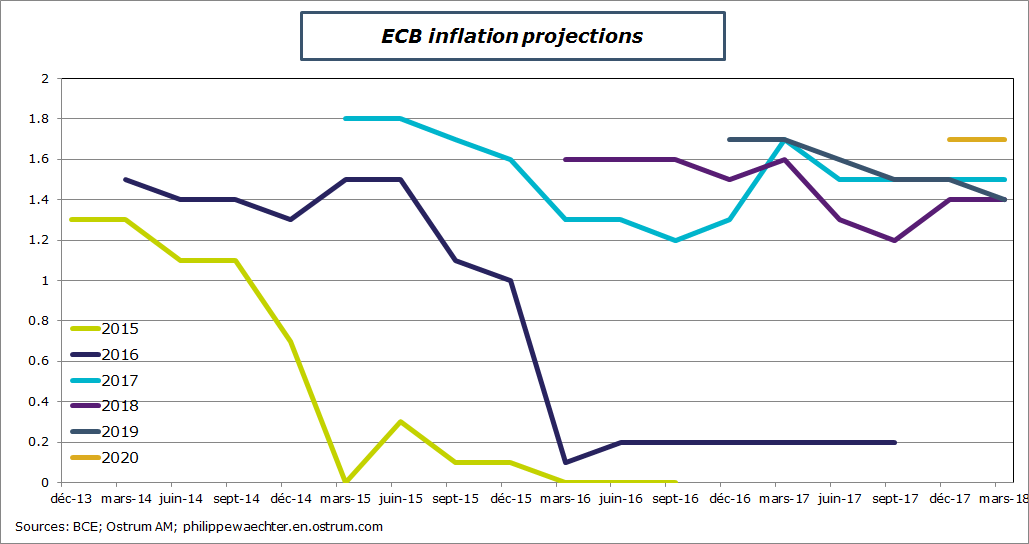

The minutes of the ECB’s March meeting reflect the central bank’s confidence in economic activity conditions in the euro area. The most noteworthy point reflecting this perception is the removal of APP easing bias i.e. the reference to increasing the asset purchase program if necessary. The bank no longer thinks that economic momentum will require emergency intervention. However, uncertainty remains on inflation trends and the ECB continues to insist that the ongoing reduction of economic slack would allow inflation to converge towards the central bank’s aim. March 2018 projections are still far from the 2% target even in 2020, when headline inflation is only expected to come to 1.7%.

Pressure on production capacity came from historically high capacity utilization rates in the first quarter of the year, both in France and in the euro area. Inadequate investment from 2011 onwards combined with austerity policies to hamper production capacities in the manufacturing sector, which did not increase as much as expected. Recent economic growth was derived from this sector via world trade in particular, so it soon hit a ceiling, which is one of the reasons why growth can no longer significantly step up a pace: production capacities cannot be markedly expanded.

Meanwhile the situation is trickier on the labor market. The landscape of the labor market has changed swiftly over the past 20 years. In the middle of the last decade, Richard Freeman explained that the arrival of China, India and Russia to the world economy had changed the capital/labor balance, increasing the cost of capital as compared to labor, as the working population doubled as a result of these three countries joining the global economy, whereas they did not bring much capital with them. The capital/labor ratio plummeted, as capital became rare, while labor grew abundant. This situation has since changed, particularly in China, which has made significant high-quality investment over recent years.

This configuration can explain decreasing wage pressure over this period, while the situation for capital ownership has improved, and could go some way to explaining the reduction in the weighting of wages in value added.

More recently, labor supply also changed vastly, but it is interesting to note that unlike globalization mentioned above, the shock was not external but rather it came from within developed countries. Labor market participation for the over-55s was previously low, but has increased rapidly over the past ten years. A recent report by the Banque de France also adds that this rise in labor market participation has dented wage inflation. In other words, greater labor market participation for this age group leads to slower wage inflation.

So overall, labor supply is increasing. We note that women’s arrival to the labor market had disrupted its balance, leading to a sharp jump in the working population during a period of robust growth, to which they were able to make a full contribution. The impact of Freeman’s “great doubling” is very different as the capital/labor ratio is completely transformed on a long-term basis due to the swift arrival of this new group. When women arrived en masse to the labor market, the trend was not as strong and the ratio did not change so extensively. Meanwhile, the recent increase in employment for the over-55s took place during a phase when investment was not so high, which made capital rare to the detriment of labor. This is one of the reasons behind sluggish wage trends.

This twofold trend was recently confirmed by another BdF report, which shows that the rise in employment in the euro area was primarily focused on the over-50s age group, while things were more difficult for those in the early and mid stages of their careers. The over-50s have seen a steady increase in employment since the first quarter of 2008, while the under-50s have suffered a decrease. This shift towards the over-50s is probably a key reason behind weak wage growth and the absence of wage inflationary pressure, combining with the increase in participation rates outlined above to explain this trend.

It is also worth noting here that the labor market has seen polarization between low-skilled and high-skilled labor (see here), while middle-skilled jobs have been hampered during this crisis period and this middle class has potentially lost a lot. Workers in the 25-50 age bracket encounter real employment difficulties if they are in the intermediate category of moderately but not highly skilled workers.

Looking to other research, a recent British report notes that falling wages have been caused by trade union decline, and this could be a contributing factor to the reduction in the weighting of worker compensation in value added. Once this mechanism has taken root, it just keeps on going and is difficult to stop. Wage share decreases as a result of the decline in bargaining power, and the effects of this decline just keep building up over time.

The question we need to raise is whether there are any ways of reversing this depressing wage trend. The combined effects of globalization, the massive change in the labor force and the loss of bargaining power do not point to a shift in trend or a swift rise in wages, so the best way to do address these challenges would be to improve productivity gains in the long term, generating a surplus that could potentially change the way value-added is shared. But for now, the western world’s innovation environment does not generate significant productivity gains, so the surplus available for sharing is smaller and the factors outlined above do not point to strong bargaining power for employees, perhaps apart from some very specific sectors (steel in Germany).

The implications of this situation are not merely economic. Recent research suggests that job market woes fuel the success of populism, and expectations of weaker employee power in the future indicate that the political balance will continue to shift, with a risk of increasing instability and the rejection of political institutions.

So we may well wonder whether the uncertainties we have seen in elections in Austria, the Netherlands and France, and more recently in Germany, Italy and Hungary are just a passing phase with a swift return to the traditional governing parties as seen in the past, or if we are witnessing the beginnings of more severe long-term political volatility? If employment trends can explain the populist vote, then we must consider the effects of recent changes on the labor market and address the possibility that uncertainties may not be about to disappear, with the ensuing risk for European integration. In this respect, Emmanuel Macron looks quite alone after recent reticence from the German government’s No. 2 .