This post is available in pdf format My Tuesday Column – 1 October 2018

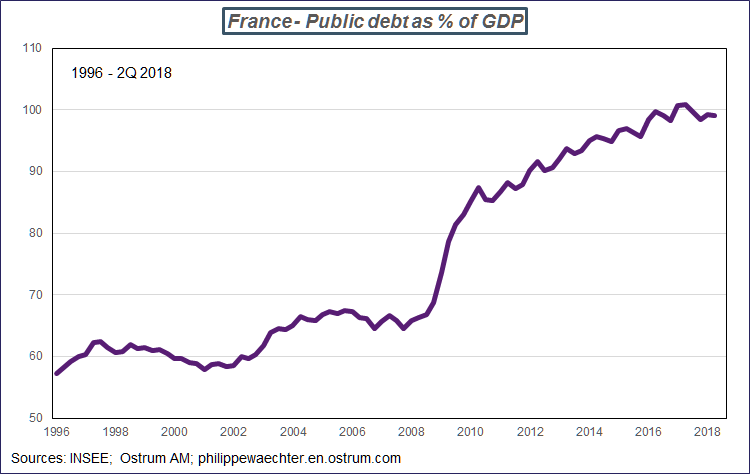

French public debt stands at close to 100% of GDP, but is this really a cause for concern?

No – it is important not to overstate the importance of this figure. French statistics body INSEE made the news as it measured public debt at over 100% of GDP for 2017, when it included railway operator SNCF’s debt. However, this is no longer the case, with debt accounting for 99% of GDP in the second quarter of 2018.

The chart shows two phases in French public debt trends – before and after the 2008 financial crisis. The State increased its debt issues and thereby smoothed the way for macroeconomic adjustment to the crisis by spreading out the shock that hit the French economy over the longer term.

We can see that the figure then rises again after 2010, but this is not a specific feature to France. It reflects slower growth in the French economy over the longer term, and a welfare set-up that failed to change to adapt to this new trend: so soaring public debt denotes a sluggish adjustment from French institutions.

In other words, the primary role of public debt is to help spread the load at times of economic shocks, but it skyrockets when the economy is slow to adjust to new economic conditions.

Is the 100% of GDP threshold a problem or not?

The figure itself is impressive and somewhat symbolic, but it is not necessarily damaging for economic momentum per se. Japanese public debt stands at 240% of GDP, yet the country has come through the financial crisis better than others judging by per-capita GDP: the country does not seem to be in danger of default.

The real problem is that we do not know just when public debt can actually become detrimental. Rogoff and Reinhart indicated in their research that public debt begins to dent growth when it moves beyond 90% of GDP, and this rule at least partly spurred on the European Commission’s austerity policy in 2011 and 2012. However, this argument does not hold water: R&R’s calculations were wrong and there is no rule on excessive public debt.

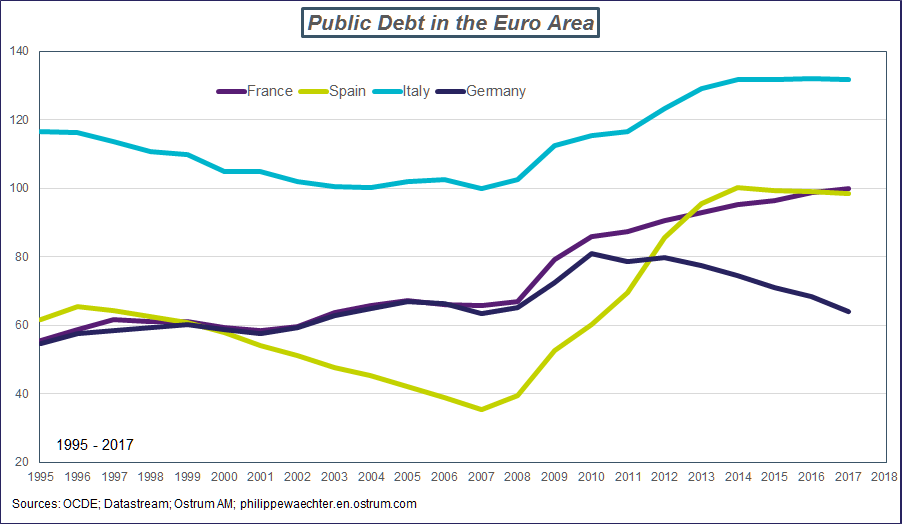

So does that mean that falling German public debt is a problem?

Germany is the only country in the euro area that was able to quickly adjust to the new post-crisis context, as it adapted to address demand from Asia.

The French economy does not have the same growth profile and it has taken longer to adjust. It is also worth noting substantial debt increases in Italy and Spain.

Is public debt vital and if so, why?

Yes, public debt is vital as it is the only asset that can transfer wealth over time while incurring no risks: it is the ultimate risk-free asset and is therefore fundamental. During the Clinton era in the late 1990s, we thought that public debt could decrease or even disappear, but that would have been a disaster.

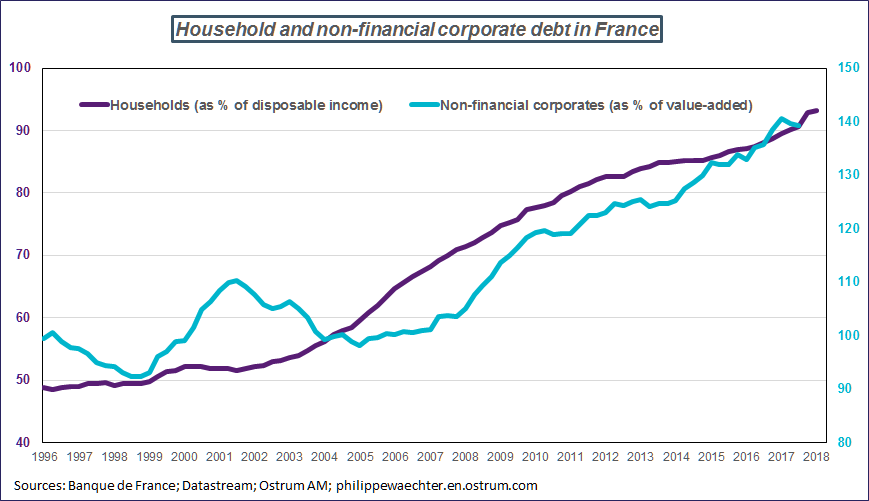

Households and companies carry debt as well as governments. Is this more worrying?

This is definitely a cause for concern in terms of what it represents as well as what it implies.

Higher household debt usually means that purchasing power is increasing more slowly and also points to very high real estate prices in cities.

Higher corporate debt may be an opportunity for some to take advantage of very low interest rates but it particularly reflects inadequate productivity gains.

Very high debt for both economic participants – households and companies – hampers their ability to adjust to a changing context, which is one of the reasons why public debt is so important in spreading out the effects of economic shocks.

So French private sector players are increasingly slow to adapt?

Yes, this reflects an overall lack of efficiency in the economic system as a whole.

What about the French 2019 budget?

We can potentially agree with a number of points, and there are two issues worth raising here. The first is that the effects of €6bn in tax cuts for households are partly cancelled out by €2.5bn in fresh levies (tobacco, carbon, etc.) as well as moves to stop indexing pensions and welfare payments to inflation. The second point is that the macroeconomic scenario looks a bit too optimistic, in my view, and expected growth of 1.7% is in the top end of the range we can expect at a time when world growth is more sluggish. This means that the 2.8% budget balance will be difficult to hit.

Prime Minister Edouard Philippe mentioned the possibility of an unemployment benefit system with regular reductions in benefits over the two-year period for higher earners – is this a good idea?

It may be, as we have seen in the past that it is usually easier for more qualified workers to get back to the job market than the overall average. Research in the 1990s showed that unemployed high earners were quicker to return to work the closer they got to the cut-off point for the reduction in unemployment benefit (this type of gradually decreasing benefits system was in place in the 1990s). However, this same trend was not observed across the board for all unemployed categories, which raises a number of questions: the first is the issue of discrimination between those who would be affected by this sliding scale and others; the second is the broader economic aspect as it is always harder to find a new job when the economic context is tough, so penalizing higher earners when jobs are scarce runs contrary to the principle of equality. There is also the issue of the actual amount of unemployment benefit itself, as it is much higher in France then in other countries amounting to a substantial proportion of the employee’s most recent wage: we may well wonder if this really an effective approach. Lastly, the so-called cadre category in France, which is a vast and varied group of more highly qualified and often managing staff including higher earners, finances 45% of the unemployment benefits system via payroll levies but only actually receives 12% of the total amounts paid out. Will they be willing to help finance a system that will not benefit them so much? It will be important to set out clear rules on these issues, but it is not entirely unreasonable to cut back benefits: any savings could be used to finance training for those who lack qualifications.

The Fed has raised its main interest rate: should we concerned about the knock-on effect on the rest of the world?

I have already discussed the Fed’s move on my blog. It is important to note that the Fed deems the current fiscal policy to be untenable and it needs to step in now – sooner rather than later – in order to avoid an accumulation of imbalances that would dent the US economy. The Fed has opted to make its moves now and keep a tight grip on the situation right though 2019 (3 hikes expected), running the risk of hampering growth rather than allowing imbalances to build up that would be more difficult to address in the long run.

There will be little knock-on effect from this move, as the US has its own very specific economic momentum: the main effect should be a stronger dollar, which will be good news for the euro area economy’s competitiveness.

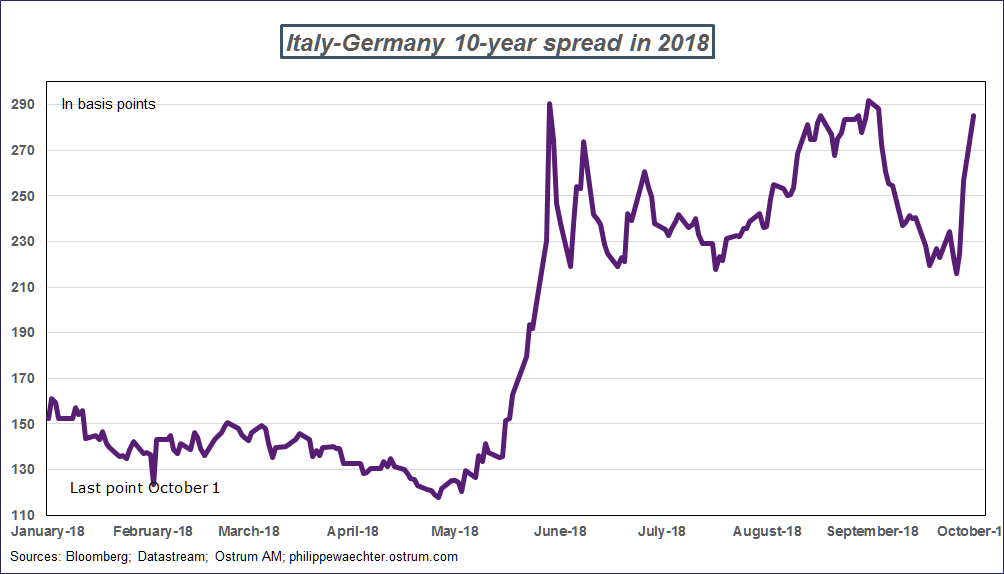

Italy has presented its 2019 budget – what should we make of that?

The deficit is set to come to 2.4% of GDP in 2019, 2020 and 2021. I wrote a long post on the matter on my blog. We should not be surprised by this announcement of a heftier deficit after the recent political watershed and the new coalition government …quite the contrary.

In an interview in Italian financial daily Il Sole 24 Ore, Economy Minister Giovanni Tria mentioned economic growth projections of 1.6% for 2019 and 1.7% for 2020. This looks somewhat excessive in light of world economic momentum, and my concern is that deficit targets will not be met, primarily as growth will be weaker as spending will probably be higher than the limited figures outlined in the budget bill. This means that the deficit could worsen towards the 3% mark or worse in 2019, or at the latest 2020. The situation would then quickly become very complicated as investors would avoid Italian debt, thereby pushing up interest rates and weakening Italian banks, which hold a lot of public debt. Non-residents account for a third of the economy’s funding, so it is important to hang onto them, otherwise Italian debt will lose a lot of liquidity.

If this happens, Italy would have to seek euro area help in the shape of the ECB and the European Stability Mechanism. It seems unlikely that Italy would leave the euro area, as it would cost a lot more than Brexit – there is the single currency to consider and the Italian economy is much weaker – and Italy does not have the required comparative advantages to help it recover quickly.